FAQ: Are Gift Cards for Employees a Tax Deduction?

Rewards can be a powerful incentive to increase motivation and morale in the workplace. You want your employees to be engaged with their jobs, and one way to help encourage that is to offer them rewards for their performance.

Picking a proper reward can be just as essential as having rewards in the first place. If your reward is too minor – pizza parties, company-branded stationery, branded travel mugs, and the like – it may not be sufficient to motivate most of your employees. Conversely, if your reward is too high – all-expenses-paid trips, $1,000 gift cards, large bonuses – it can draw attention to under-compensation amongst your workers.

At a reasonable scale, money is often one of the best possible extrinsic rewards. Too little and it feels insulting, while too much can feel out of proportion and cause other issues; properly-scaled monetary rewards are the most flexible and beneficial incentives.

When giving monetary rewards like gift cards to your employees, are there tax implications?

A common concern amongst employees is that monetary rewards get taxed, and if they’re right on the edge of an income tax bracket, it could have negative repercussions. This concern is valid, but it isn’t accurate – tax brackets only tax income within their limit and don’t affect money earned up to their minimum range – but there are tax implications for gift cards and other monetary rewards.

Let’s run through common questions and concerns and get to the bottom of the tax implications of gift cards.

Note: Before we begin, keep in mind that this information applies to the United States tax situation and will vary if your business is based in another country. It is also primarily concerned with federal taxes; state taxes will be a different story and will vary from state to state. Finally, tax regulations can evolve, and what is accurate now may not be in the future. Tax regulations have already changed once in recent years.

Can You Deduct the Cost of Gifts to Employees?

First off, can you deduct gifts at all? After all, if you can’t deduct the cost of those incentives to your employees, then it won’t matter whether it’s a gift card or another form.

The answer is yes, with qualifications. You are allowed to deduct all, or part, of the costs of a gift, up to a specific limit per employee.

That limit is $25 per employee per tax year. There are, however, some other restrictions. Here’s what the IRS has to say about it:

“Incidental costs such as engraving, packing or shipping aren’t included in the $25 limit if they don’t add substantial value to the gift.

For purposes of the $25 per person limit, don’t consider gifts costing $4.00 or less that have your business name permanently engraved on the item and which you distribute on a regular basis.

Any item that could be considered either a gift or as entertainment is generally considered entertainment and cannot be deducted.”

In other words, certain value-adds will increase the value of the gift, but minor additions like company branding are generally considered incidental and do not.

You might notice that this doesn’t seem applicable to gift cards. After all, a gift card – branded or not – is still just a form of money, not a tangible gift or piece of entertainment.

Do Gift Cards Count as Cash, Wages, or Gifts?

The IRS considered gift cards to be gifts, up to the $25 limit. However, this has recently changed, and now any form of money is considered money. This distinction comes down to the rules of “de minimis fringe benefits.” More on those in a moment.

Under the current IRS regulations, any monetary compensation is considered wages and is thus regarded as taxable, whether in a paycheck, a cash bonus, or a gift card. It doesn’t matter what purpose the money has; it’s taxable if it’s unrestricted money.

The exception is if the money is used for a specific item. A voucher for a meal from the workplace cafeteria, even if the meal has a defined price, is considered fringe; a gift card to a local restaurant with an equivalent cash value is considered compensation instead.

More on this later in the post.

Here’s the relevant quote from the IRS in sections 1.132-6:

“Cash or cash equivalent items provided by the employer are never excludable from income. An exception applies for occasional meal money or transportation fare to allow an employee to work beyond normal hours. Gift certificates that are redeemable for general merchandise or have a cash equivalent value are not de minimis benefits and are taxable.”

So, unrestricted money is not tax-deductible.

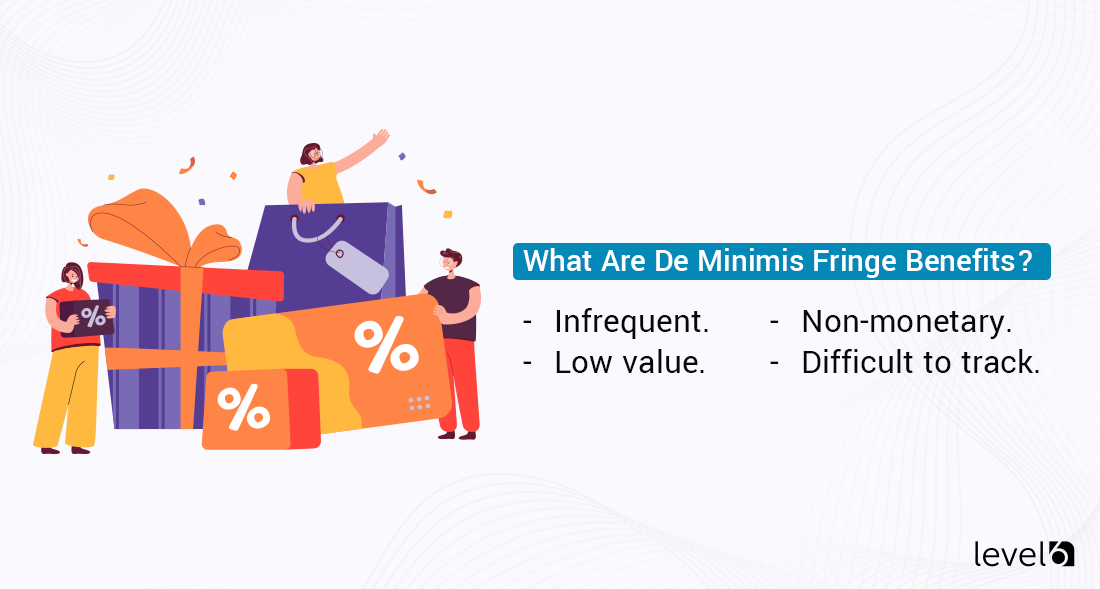

What Are De Minimis Fringe Benefits?

The IRS deems specific amounts of gifts to be “de minimis fringe benefits,” or in other words, small, low-value benefits that are simply incidental to doing business. For employee incentives to be considered de minimis fringe, they must be:

- Regular benefits or recurring benefits are not incidental or occasional.

- Low value. There’s no set value to cap for de minimis fringe benefits; however, the IRS has previously ruled that $100 is not de minimis, and you can assume that the limit is likely even lower.

- Non-monetary. Any gift that is cash or cash-equivalent cannot be considered de minimis.

- Difficult, unreasonable, or impractical to track.

The point of de minimis fringe benefits is to allow businesses to ignore little gifts that would create sizeable administrative overhead for comparatively little gifts. It’s a codified way for the IRS to say “don’t worry about it” to minor, incidental gifts and occasional rewards.

The IRS lists several examples of what can be considered de minimis fringe benefits. These include occasional use of an office photocopier, a few snacks and some coffee, flowers, fruit, and books given as infrequent gifts, and the personal use of an employer-provided cell phone.

Tracking any of these requires a high degree of granularity and would generally only result in pennies worth of tax burden while spending dozens of employee-hours tracking and processing. It’s not worth it for the IRS or your business, so it’s written off.

You don’t even need to report that you have de minimis fringe benefits; it’s just assumed. However, if you are found to be exploiting this and giving gifts too regularly while writing them off as de minimis fringe benefits, you may be subject to an audit and penalties from the IRS.

Again, however, this all applies to physical gifts and other tangible items. Gift cards are generally just a form of money and are never considered de minimis gifts.

How Did the Rules Change?

Above, we mentioned that the rules changed recently. That rules change recategorized monetary and cash-value rewards, like gift cards, as compensation or wages rather than gifts.

Previously, you could consider gift cards as fringe benefits and write off up to $25 per employee per year. Now, you cannot write off any of that value.

Per SHRM:

“In the past, employers could give employees cash or a cash equivalent gift such as a gift certificate for amounts less than $25 without any tax concern. These were known as de minimis fringe benefits or gifts.

That is no longer the case. The Internal Revenue Service (IRS) tells employers that all cash gifts, including gift cards, are considered taxable wages unless specifically excluded by a section of the Internal Revenue Code (IRC).”

This change allowed the IRS to streamline much of small business accounting, reducing overhead for themselves and companies.

What About Awards?

Sometimes, you may want to give an employee a special reward – for example, a tenth work anniversary award or a high-performance award for the employee of the year. These awards can be written off and are tax-deductible, assuming they are tangible personal property.

In other words, you can give an employee a $400 watch as an award for length of service with the company, and the value of that watch can be tax-deductible. However, you cannot award them a $400 gift card and write that off; as money, it must be reported as income. As the IRS says:

“Cannot be cash, cash equivalent, vacation, meals, lodging, theater or sports tickets, or securities.”

Additionally, the award must be presented as part of a meaningful presentation, such as an award service ceremony. Something just left on an employee’s desk is not sufficient.

You can read more about this in IRS documentation, such as publication 535.

How Should Gift Cards be Reported?

If you’re giving gift cards as cash rewards to your employees, you need to report them as income. It doesn’t matter if they’re sporadic, one-time rewards, or regular awards based on monthly performance. It also doesn’t matter if they’re unrestricted cash cards or cards used for specific items, like gas cards or food cards. As long as gift cards have an equivalent cash value – usually stated on the back of the card, in many cases – it is taxable as income.

This money should be tallied up as if it were cash added to the monetary compensation your employee earns over the tax year. It should be included as wages on their W-2 and is subject to income tax withholding, just as any other form of monetary compensation.

Can a Gift Card Push an Employee into a Higher Tax Bracket?

Tax brackets are a concern for certain employees, but they shouldn’t be. The answer is yes and no.

Yes, if an employee is right at a threshold where higher compensation will put them in a higher tax bracket, a gift card will do so – this is because a gift card is considered income from the perspective of the IRS.

However, this generally should not be a concern. Tax brackets work in your favor because they only apply to money earned within that bracket. While the employee may have a higher tax bracket for the gift card’s value, it only applies to the value of that gift card. It does not affect the tax rate for prior compensation.

Thus, if your employees are worried about the tax implications of a gift card, you can reassure them that it will not cause them to lose money. At most, it may mean the net value of the gift card is slightly lower than it appears, but that’s all.

Are Gift Cards Still Worth Giving?

Some companies in the past have used gift cards to hide some small amount of compensation and take advantage of gift write-offs per employee.

The only tax deduction you can use as a business, as far as gifts are concerned, is the $25 per employee per year limit. This limit applies primarily to gifts that are relatively easy to track.

Gifts will fall into one of three categories:

- If it’s burdensome and sporadic to track, it falls under the de minimis category and does not need to be reported.

- If it’s easy to track and non-cash or cash-equivalent, up to $25 of the value can be deducted from your business taxes.

- If it’s cash or cash-equivalent, it cannot be deducted and must be taxed as income.

Despite the tax burden of cash-equivalent gifts such as gift cards, it’s still worthwhile to offer them as a potential reward. Monetary rewards are the most flexible and most valuable to the most significant number of employees. They are one of the best forms of incentive you can leverage to improve performance and motivation in the workplace.

We’re here to help you create an incentive program specifically designed for your company. All you need to know is what kind of incentive you might want to provide, how many employees will receive it, and the total payout scale. If you’re curious about the pricing, take advantage of our pricing calculator. From there, we’ll contact you with details and can help you design a program that’s just right for you.

Do you have any questions for us? Are you thinking of implementing gift cards for your employees, or do you have any questions for us? Feel free to leave a comment or give us a call today to see how we can help!