Quick Answer: What Is Distributor Rebate Accrual and Why Does It Matter?

Distributor rebate accrual is the process of estimating and recording the rebates a manufacturer expects to owe distributors, recognizing revenue net of that estimate at the point of sale. Under ASC 606, these rebates are variable consideration — accurate accrual prevents costly revenue misstatement.

Why Distributor Rebates Are Variable Consideration Under ASC 606

Distributor rebates are variable consideration under ASC 606 because the final amount a manufacturer collects is contingent on a future event — typically the volume a distributor ultimately purchases. The standard treats them as part of Step 3, determining the transaction price, and requires revenue to be recognized net of the expected rebate from the moment the sale occurs.

Deloitte’s guidance is explicit on this point: an amount of consideration can vary because of “discounts, rebates, refunds, credits, price concessions, incentives, performance bonuses, penalties, or other similar items” under ASC 606-10-32-6 (Deloitte DART). A retrospective volume rebate is variable consideration because the entity’s entitlement to consideration for each unit sold is contingent on the occurrence of a future event.

The practical consequence is that revenue is recognized net, not gross. KPMG notes that if a manufacturer intends to provide an incentive, or the customer can reasonably expect one, “an estimate of the incentive is included in the transaction price and recorded as a reduction of revenue when the related good is sold to the distributor rather than waiting until the offer is made” (KPMG).

This is the single most important distinction in rebate accrual accounting: the liability is built as sales occur, not when a check is cut. Booking distributor rebates to SG&A or COGS — rather than as a revenue reduction — is the first accounting error we see in nearly every manual program we evaluate, as both Grant Thornton and RSM confirm.

IFRS 15 reaches the same outcome, applying a “highly probable” threshold to the constraint rather than ASC 606’s “probable,” but the core principle — estimate and recognize net — is identical (IFRS Foundation). The International Accounting Standards Board (IASB), which issued IFRS 15 jointly with FASB, designed both standards to converge on the same economic outcome for variable consideration. For global manufacturers, the distributor rebate accrual process is broadly the same even as statutory language differs across jurisdictions.

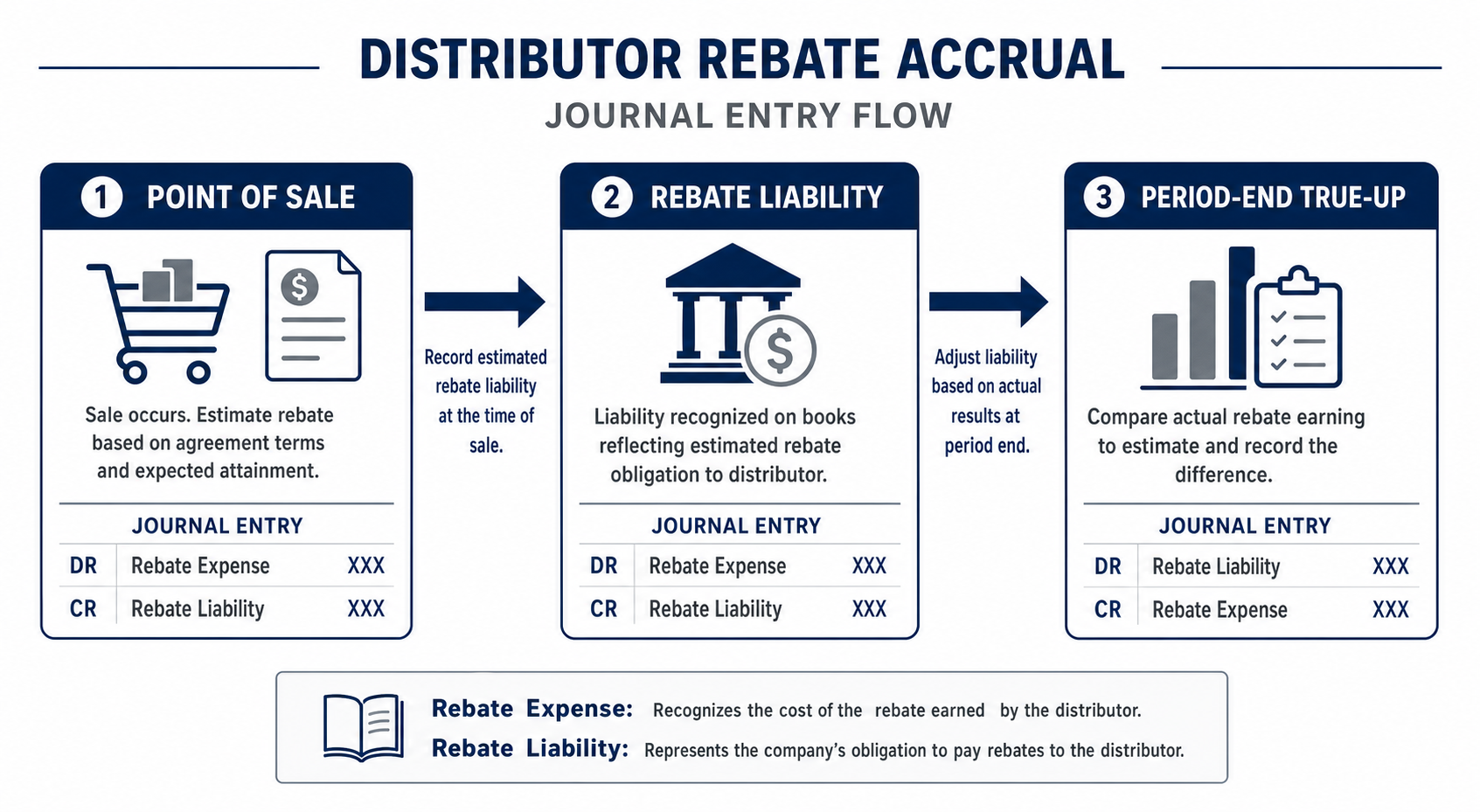

The Distributor Rebate Accrual Journal Entry

The core distributor rebate accrual journal entry records full receivables, recognizes revenue net of the estimated rebate, and credits a separate rebate liability. This keeps the income statement honest while parking the estimated payback in a clearly identifiable balance-sheet account.

At the point of sale, assume a manufacturer ships $100,000 of product to a distributor and estimates a 3% rebate ($3,000) will ultimately be earned:

| Account | Debit | Credit |

|---|---|---|

| Dr. Accounts Receivable (full invoice) | $100,000 | |

| Cr. Revenue (net of estimated rebate) | $97,000 | |

| Cr. Rebate Liability (estimated rebate) | $3,000 |

Note that the receivable is recorded at the gross invoice amount because the distributor still owes the full price; the rebate is a separate obligation the manufacturer expects to settle later. The rebate liability accrual is the credit that bridges the gap between gross billing and net revenue.

When the rebate is later paid or applied as a credit memo, the liability is cleared:

| Account | Debit | Credit |

|---|---|---|

| Dr. Rebate Liability | $3,000 | |

| Cr. Accounts Receivable (or Cash) | $3,000 |

The true-up happens at period-end when the actual or revised estimate diverges from what was accrued in the distributor rebate accrual. If the distributor’s trajectory now points to a 4% rebate on the same $100,000 in sales, the manufacturer must record an additional $1,000 and reduce revenue in the current period:

| Account | Debit | Credit |

|---|---|---|

| Dr. Revenue (adjustment for under-accrual) | $1,000 | |

| Cr. Rebate Liability | $1,000 |

Critically, changes in estimate flow through the current period — they are not a retroactive restatement of prior periods. Deloitte confirms that at the end of each reporting period the entity updates the estimated transaction price under ASC 606-10-32-14, accounting for the change prospectively (Deloitte DART).

How to Estimate the Accrual Amount: Expected Value vs. Most Likely

ASC 606 permits two estimation methods for distributor rebate accrual, and the manufacturer must choose whichever better predicts the consideration it will ultimately be entitled to. The expected value method suits portfolios with many possible outcomes; the most likely amount method suits binary or near-binary outcomes.

Under ASC 606-10-32-8, the expected value method is “the sum of probability-weighted amounts in a range of possible consideration amounts” and may be appropriate when an entity has a large number of contracts with similar characteristics (Deloitte DART). The most likely amount method picks the single most likely outcome and fits a contract with only two possible results (Grant Thornton).

Tiered vs. Flat-Rate Accrual Mechanics

A flat-rate program is straightforward: a 2% rebate on all purchases simply requires a 2% reduction in recognized revenue for every sale. Tiered programs — for example, 2% on the first $1M, 4% on $1M–$5M, and 6% above $5M — require more sophisticated estimation. If historical data suggests a specific distributor typically reaches the 4% tier, the distributor rebate accrual should reflect that blended expected rate from the very first invoice, not only once the distributor crosses the $1M threshold.

A multi-tier volume program illustrates the estimation choice. RevenueHub’s case study describes a manufacturer offering $0 below 100 meters, a $500 rebate for 100–10,000 meters, and $800 above 10,000 meters, with over 99% of distributors expected in the first tier (RevenueHub). Because the outcome was binary at the contract level, the manufacturer used the most likely amount — setting the transaction price at $4,500 stated price less the $500 expected rebate, or $4,000.

A vital nuance: the standard does not default to the maximum discount. KPMG is direct — “the new standard does not default to the maximum discount but requires companies to evaluate the probability and significance of a reversal of revenue to determine the estimated discount” (KPMG). Manufacturers that reflexively accrue at the top tier systematically understate revenue.

Estimates are not static. KPMG instructs companies to estimate volumes and the resulting discount, then update “that estimate throughout the term of the contract,” with the estimate refreshed “each reporting period until the uncertainty is resolved” (KPMG). Grant Thornton’s comprehensive ASC 606 guide reinforces continuous reassessment of variable consideration through the contract term (Grant Thornton).

Rebate Agreement Terms That Change the Accrual

The accuracy of any distributor rebate accrual depends directly on how well the agreement terms are captured in the estimation model. Six contract fields drive most of the accrual math: eligibility basis (which products or SKUs qualify), volume thresholds and tier breakpoints, retroactive vs. incremental rebate logic, effective dates and program-year boundaries, claim submission windows, and payment or credit-memo settlement terms.

Retroactive logic is particularly consequential: when a distributor crosses a tier threshold, the higher rate applies to all prior-period qualifying purchases, not just incremental volume. This means a single threshold crossing can require a retroactive revenue adjustment on months of previously recognized sales — which is why monitoring distributor volume trajectories throughout the year, not just at year-end, is a compliance requirement, not merely a best practice.

Period-End Reconciliation: What Manufacturers Must Check

At every period-end, manufacturers must reconcile the distributor rebate accrual balance against active program agreements and update each estimate for the latest volume data. A rigorous, repeatable process ensures the rebate liability accrual never drifts away from economic reality — and that the balance can be defended to auditors.

We call this the Four-Tie Reconciliation, and we apply it to every distributor rebate accrual balance at close:

- Tie to agreements. Match every open rebate liability balance to a current, signed program agreement and its tier structure. Any liability without a live agreement is a candidate for reversal.

- Tie to volume. Pull actual cumulative purchases by distributor and recompute the most-likely tier or the probability-weighted estimate. ASC 606-10-32-14 requires this update each reporting period (Deloitte DART).

- Tie to payments. Reconcile rebates already paid or credited against the liability to confirm settled amounts cleared the correct account and period.

- Tie to the true-up. Post the current-period revenue adjustment for any gap between the refreshed estimate and the carrying liability, recognizing the change prospectively rather than restating.

Quarterly Reassessment Triggers

We recommend establishing explicit quarterly reassessment triggers to force a systematic review of purchasing run rates against established targets. If a distributor’s volume is falling significantly behind schedule, the rebate liability accrual must be adjusted downward — releasing deferred revenue back to the income statement. If a distributor’s velocity accelerates midway through the year, the accrual rate must increase to reflect the higher anticipated tier. Without these scheduled reassessments, the liability account becomes dangerously disconnected from reality.

Disclosure matters here too. Grant Thornton’s guide details the ASC 606 requirement to disclose information about the methods, inputs, and assumptions used to estimate variable consideration and to assess the constraint (Grant Thornton). RSM similarly highlights that manufacturers face heightened estimation and disclosure demands around customer incentives and rebates (RSM).

The Claim-to-Settlement Workflow

Understanding how a distributor rebate accrual clears the balance sheet requires mapping the full operational workflow from qualifying sale to final payment. The sequence has five stages: qualifying sales accumulate against agreement eligibility and threshold rules; the manufacturer calculates the earned rebate and generates a claim or credit memo at period-end; the claim moves through an approval workflow where finance verifies volume data and program managers confirm eligibility.

Upon approval, the rebate is paid via ACH, check, or applied as a credit against the distributor’s receivable balance. The rebate liability is then relieved and any residual over- or under-accrual is trued up through current-period revenue.

Delays or gaps at any stage — a disputed volume figure, a late claim submission, an unapproved credit memo — leave the rebate liability accrual open longer than necessary and increase the risk that the balance drifts from the actual obligation. A disciplined claim-to-settlement workflow is therefore inseparable from accurate distributor rebate accounting.

Common Over- and Under-Accrual Errors (Checklist)

Most distributor rebate accrual failures trace back to six recurring errors. Each distorts revenue, and each has a clean correction. We see these in nearly every manual program we evaluate.

- 1. Treating the rebate as an expense. Booking rebates to COGS or SG&A overstates both revenue and operating costs. Correction: rebates are a reduction of the transaction price — a reduction of revenue, not an expense (KPMG; RSM).

- 2. Accruing at payment date. Waiting until the rebate is paid front-loads revenue and back-loads the hit. Correction: accrue at the point of sale and ratably as purchases accumulate (KPMG).

- 3. Using the maximum tier rate. Defaulting to the top discount overstates the liability and understates revenue. Correction: estimate the most likely amount or probability-weighted value based on historical data and current trajectories — never the maximum by default (KPMG).

- 4. Failing to reassess quarterly. Setting an accrual rate in January and ignoring it until December guarantees a painful year-end true-up. Correction: implement a mandatory quarterly reassessment trigger to catch shifting volume trends and adjust the distributor rebate accrual accordingly (Deloitte DART).

- 5. Not reconciling the liability account. Balances that aren’t tied to live agreements accumulate as untracked over-accruals — an unauditable “slush fund.” Correction: require a monthly roll-forward schedule matching the distributor rebate accrual balance to calculated program obligations for each distributor.

- 6. Missing the true-up. When actual rebates differ from accrual, the gap lingers on the ledger. Correction: post the current-period revenue adjustment immediately upon final settlement, recognizing the change prospectively (Deloitte DART; RevenueHub).

Anonymized Example: A Mid-Market Industrial Manufacturer

We worked with a mid-market industrial components manufacturer running tiered rebates across roughly 140 distributors. Before reform, finance accrued at the maximum 5% tier across the board and trued up only at year-end, producing a chronically overstated rebate liability accrual.

The before state: a year-end rebate liability carried at roughly $4.2 million against actual rebates earned of about $2.6 million — a 62% over-accrual that depressed reported revenue by approximately $1.6 million during the year and forced a large, lumpy fourth-quarter true-up. Audit adjustments and disclosure questions followed.

The after state: by switching to a probability-weighted estimate per distributor, reassessing monthly, and applying the Four-Tie Reconciliation at each close, the manufacturer brought its accrued liability to within roughly 4% of actual earned rebates. Quarterly revenue smoothed out, the year-end true-up shrank from seven figures to immaterial, and the audit cycle moved faster because every balance traced to a live agreement and a documented estimate.

What a Rebate Management Platform Tracks That Spreadsheets Miss

Spreadsheets struggle with distributor rebate accounting because they cannot continuously reconcile estimates to live volume, agreements, and payments at scale. A purpose-built platform maintains a real-time accrual that finance can trust at any moment, not just at quarter-end.

Three capabilities separate a managed platform from a workbook. First, a real-time accrual rate by distributor that recalculates as each order posts, so the rebate accrual journal entry reflects current volume rather than a stale assumption. Second, automated tier-progression triggers that flag when a distributor is approaching or crossing a threshold, prompting the most-likely-amount reassessment the standard demands. Third, a complete audit trail that ties every accrued dollar to an agreement, a volume record, and a settlement — the backbone of the Four-Tie Reconciliation and a direct answer to the disclosure expectations Grant Thornton describes (Grant Thornton).

ERP Integration and Accrual Automation

Reliable distributor rebate accrual at scale requires three data integration points: source transactions from the order management or ERP system (to feed real-time volume against agreement thresholds), agreement master data (tier structures, effective dates, retroactive logic, claim windows), and a clean posting path to the general ledger so accrual entries, true-ups, and liability reliefs flow into the correct accounts without manual rekeying. When these three feeds are automated and reconciled, the close process shrinks from days to hours and audit support becomes a reporting query rather than a manual reconstruction.

Level 6’s channel sales incentive solutions include real-time performance dashboards and configurable reward structures that give finance and program teams a shared, current view of distributor rebate performance. For program mechanics, our explainer on how the rebate process works walks through submission to settlement. Our overview of volume incentive rebate programs covers the program design decisions that upstream affect accrual complexity, and our guide to fraud risks in channel incentive programs covers the verification controls that keep accruals clean.

Final Takeaways

Accurate distributor rebate accrual comes down to four habits: recognize revenue net of the estimated rebate at the point of sale, estimate with the right method rather than the maximum tier, reassess every reporting period, and reconcile the liability to live agreements at every close. Done well, distributor rebate accrual eliminates lumpy true-ups and stands up to audit scrutiny.

- Distributor rebates are variable consideration under ASC 606 and IFRS 15 — revenue must be recognized net of the estimate at the point of sale.

- Two estimation methods exist — expected value for broad portfolios, most likely amount for binary outcomes. Never default to the maximum tier.

- Quarterly reassessment is mandatory — stale estimates and missing true-ups are the primary drivers of year-end revenue surprises.

- The Four-Tie Reconciliation — tie to agreements, volume, payments, and the true-up — is the repeatable process that keeps the liability defensible.

- Platform tracking replaces spreadsheet risk — real-time accrual, tier-progression triggers, and a full audit trail are what compliant rebate accrual accounting requires at scale.

The accounting is only as good as the operational data feeding it. If your rebate accrual accounting still relies on spreadsheets and year-end catch-ups, the gap between estimate and reality is almost certainly larger than you think. Talk to a Level 6 strategist about building a distributor rebate program your finance team can reconcile with confidence.

Frequently Asked Questions

These are the questions finance teams and controllers ask most often when setting up or auditing a distributor rebate accrual process.

What is a distributor rebate accrual?

A distributor rebate accrual is the estimated liability a manufacturer records for rebates it expects to owe distributors based on their purchase volume. Under ASC 606, the manufacturer recognizes revenue net of this estimate at the point of sale and credits a rebate liability, rather than waiting until the rebate is actually paid (KPMG).

How is a rebate different from a discount under GAAP?

Both reduce the transaction price, but timing and certainty differ. A standard discount is typically fixed and applied at invoice, while a retrospective volume rebate is variable consideration whose final amount depends on a future event. ASC 606 requires manufacturers to estimate the rebate and recognize revenue net of it as sales occur (Deloitte DART).

When should a manufacturer accrue a distributor rebate?

The accrual begins at the point of sale, building ratably as the distributor’s qualifying purchases accumulate. KPMG’s guidance is clear that the estimated incentive is recorded as a reduction of revenue when the goods are sold to the distributor, not when the rebate offer is made or paid (KPMG).

What account does a rebate accrual go on the balance sheet?

The estimated rebate is recorded as a rebate liability — a credit balance carried among current liabilities until it is paid or applied. The offsetting entry reduces revenue, not an expense account, which keeps the income statement consistent with the net transaction price required under ASC 606 (KPMG).

What is the difference between over-accrual and under-accrual of a rebate?

Over-accrual records a larger rebate liability than will be earned, understating revenue; under-accrual records too little, overstating revenue and forcing a later downward adjustment. Both are corrected through a current-period true-up when estimates are reassessed — not by restating prior periods (Deloitte DART).

How does ASC 606 affect distributor rebate accounting?

ASC 606 classifies distributor rebates as variable consideration in Step 3 of the five-step model, requiring revenue to be recognized net of an estimated rebate, subject to the constraint against significant revenue reversal. The standard does not default to the maximum discount and requires reassessment each reporting period (KPMG; Grant Thornton).

How often should manufacturers reconcile their rebate liability accounts?

At minimum every reporting period, because ASC 606-10-32-14 requires the estimated transaction price and the constraint to be updated at the end of each period. We recommend monthly reassessment of volume and a full Four-Tie Reconciliation tying the liability to active agreements, payments, and the true-up at each close (Deloitte DART).

What happens if a distributor does not hit the tier threshold?

If a distributor falls short of a higher rebate tier, the manufacturer reverses the over-accrued portion of the liability and recognizes additional revenue in the current period. Because changes in estimate are prospective under ASC 606, the adjustment flows through the period in which the new information arises — not as a restatement of prior-period revenue (Deloitte DART).

Do manufacturers with large distributor networks really need rebate management software?

For any manufacturer running tiered distributor rebate accrual across more than a handful of partners, dedicated software is almost always justified. Spreadsheets cannot continuously apply retroactive tier logic, flag threshold crossings, or generate audit-ready accrual rollforwards at scale. The operational cost of manual close processes — and the audit exposure from undocumented estimates — typically exceeds software cost well before a network reaches 20 active rebate agreements.

How do retroactive rebate tiers affect accruals across multiple distributor branches?

When a manufacturer aggregates volume across a distributor’s branch network to determine tier eligibility, the rebate liability accrual must reflect the combined purchasing trajectory of all branches — not each branch in isolation. A branch that appears unlikely to hit a threshold independently may cross it on an aggregated basis, triggering a retroactive rate adjustment across all qualifying sales for every branch in that entity.