Did you know that the average American has two to three credit cards? According to the Guinness Book of World Records, the biggest collection of valid credit cards is held by Manish Dhameja. As of April 2021, he holds a stunning 1,638 credit cards.

According to Dhameja:

“I think my life was incomplete without credit cards. I just love credit cards. I enjoy complimentary traveling, railway lounge, airport lounge, food, spa, hotel vouchers, complimentary domestic flight tickets, complimentary shopping vouchers, complimentary movie tickets, complimentary golf sessions, complimentary fuel, etc., by reaching milestones and using rewards points, air miles, and cashback.”

We certainly don’t recommend you follow his lead, but having multiple credit cards can be an effective way to manage an important factor credit bureaus use to determine your creditworthiness. Your credit utilization ratio. This is the “percentage of your total credit used from the total credit available to you.”

Bankrate lists eight different types of credit cards and suggests you choose the right ones for you depending on your spending and financial goals. Their list includes the following:

- Rewards credit cards “reward” you with points or cash back based on a specified percentage of your spending.

- Cashback credit cards make it easy to earn cash back…on your spending.

- Travel credit cards allow you to earn rewards toward travel spending, including how you get to where you’re going and where you stay once you arrive.

- Business credit cards let you keep your personal and business spending separate, which makes your business accounting easier.

- Student credit cards are a helpful way to start using and building a credit history, as they are geared toward young people who have yet to offer a credit history.

- Secured credit cards require you to put down a deposit in order to be extended a line of credit, which is often helpful in rebuilding or repairing your credit score.

- Store-branded (or private-label) credit cards are offered by retail stores or restaurants and can usually only be used at the store or restaurant that offers the card.

Let’s discuss some of these co-branded cards, as well as their pros, cons, and differences!

Co-Branded Credit Cards

The final type of credit card is a co-branded card. This type of card is a hybrid between store and rewards cards. This refers to the fact that the card is co-branded with a major network or an issuer of credit cards. This lets the card owner use them anywhere credit cards are accepted.

Many of us have one of these co-branded cards in our collection of credit cards as it’s becoming increasingly common for retailers, hotels and airlines, etc.) to partner with:

- A card network like Visa or Mastercard

- A bank like Chase or Capital One

- A network/issuer like Discover and American Express

What’s the difference between a credit card network and a credit card issuer? Credit card networks and issuers “play very different but essential roles” in working your credit card. Working together, they process transactions from bank to bank and facilitate where your card can be used.

The role of a card network is to “facilitate transactions between merchants and card issuers.” These networks create virtual payment infrastructures and charge merchants interchange fees to process consumers’ credit or debit cards.

Credit card issuers are “financial institutions that provide cards and credit limits to consumers.” The issuer manages many aspects of credit cards, including the application and approval process, distributing cards, deciding terms and benefits (such as rewards and annual fees), collecting payments from cardholders, etc.

The co-branded credit card can be used at any location as long as you shop within the “network of affiliates.” You can use earn “loyalty points, perks, and deals” by shopping at the “sponsoring retailer,” and these cards are more versatile than a store (or private label) credit card.

The rise of digital payments, especially for younger adults and millennials, has recently caused an increase in those demographics choosing co-branded credit cards. Reporting by A Packaged Facts shows that “nearly 29% of U.S. adults (73.7 million people) now own co-branded credit cards.”

Their findings feel these cards “allow both parties to optimize the best of both worlds—an integrated customer base and a vibrant sales channel…[and] allow both parties to optimize the best of both worlds—an integrated customer base and a vibrant sales channel.”

Other benefits to retailers and service companies include card-sharing revenue and monetization models that fairly distribute their “individual revenue sources” between partners. The cards also provide more complete customer data and increase both parties’ brand visibility.

How Do Co-Branded Credit Cards Work?

Co-branded credit cards work by creating a partnership between a retailer and a bank or financial institution. Examples of these types of cards include:

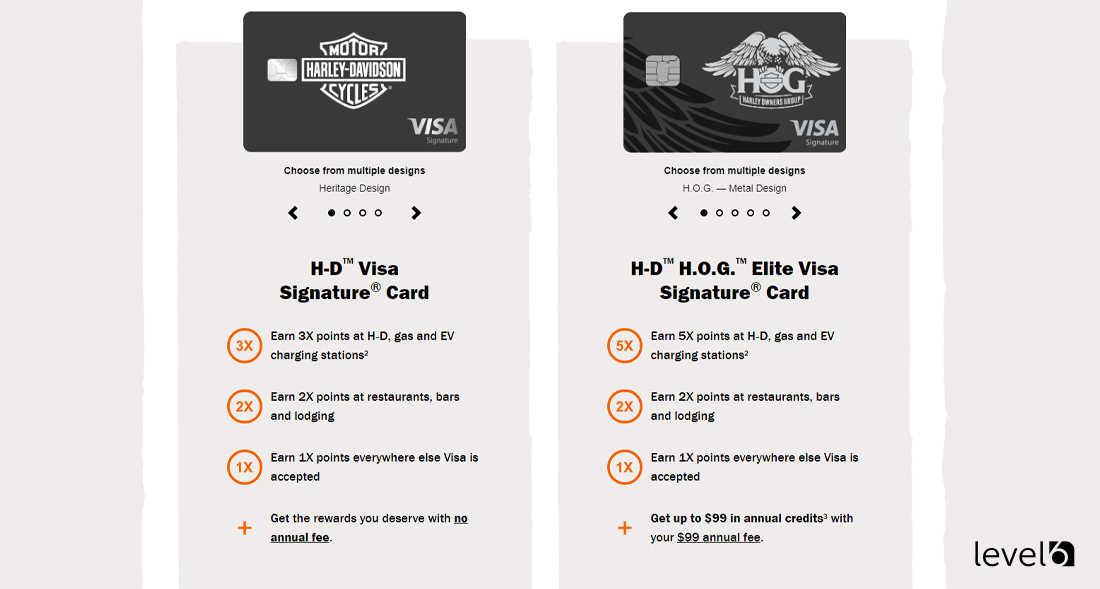

- Harley Davidson Visa Signature Card

- Korean Air SKYPASS Visa Signature

- Kroger Rewards World Elite Mastercard

You can use the Harley Davidson and SKYPASS credit card anywhere Visa is accepted, and the Kroger Mastercard anywhere Mastercard is accepted. Plus, you’ll be incentivized to spend at the specific retailer in order to earn points or other perks.

When using a co-branded credit card, you are responsible for making your payments and adhering to the terms of use. Late payments will result in fees and penalties, as with any other credit card.

When you use the card at the partner’s store, you’ll receive additional rewards based on the agreement between the two companies. Depending on the agreement, these rewards may come in the form of cashback, points, or miles.

You may also be eligible for additional rewards and benefits through the partner’s loyalty program. For example, if you have a co-branded airline credit card, you may be eligible for priority boarding, free checked bags, or lounge access.

With a co-branded credit card, you get access to the rewards and benefits the credit card issuer and the partner offers. This makes it easier to optimize your spending and enjoy additional perks while shopping.

If you’re trying to decide which co-branded credit card is right for you, make sure to read all the fine print and compare offers from different issuers. That way, you can make sure that you’re getting the best possible deal.

Additionally, consider what rewards will best match your lifestyle and needs. If you travel often, focus on cards with travel-related bonuses such as bonus miles or discounts on rental cars and hotels.

If you frequently shop at a certain retailer, look for cards that give bonus rewards or discounts at their stores. Also, think about how often you’ll be able to take advantage of the rewards offered.

Some cards may only be useful once or twice a year, so make sure they fit your budget and lifestyle. With careful research, you should be able to find the right co-branded credit card to help maximize your spending.

Benefits Of Using A Co-Branded Credit Card

One of the main advantages of a co-branded credit card is that it gives cardholders more control over their spending. With a co-branded card, you can earn bonus points or cashback rewards for purchases made with the card at specific retailers or restaurants. You may also be eligible for additional discounts and benefits when you use the card to make purchases from the co-branding partner.

Another benefit of a co-branded credit card is that it can help improve your credit score. By using your co-branded credit card responsibly and paying your balance in full each month, you can demonstrate to lenders that you are responsible with credit and build up your credit score over time.

Additionally, some co-branded cards offer travel benefits like complimentary hotel stays and airline tickets. These benefits vary by card and often come with additional rewards and incentives like discounts on airfare and hotels and other perks like priority boarding and access to exclusive lounges.

Finally, if you are a frequent customer of the partner brand, a co-branded credit card can be a great way to maximize the value of your loyalty program. Many times these cards come with higher earning potential than traditional credit cards, allowing you to get the most out of your loyalty program.

Overall, co-branded credit cards offer a wide range of benefits, making them an attractive option for savvy shoppers and travelers. From increased spending control to improved credit scores and access to exclusive loyalty programs, these cards can be a great way to maximize your spending.

Plus, with no annual fee and relatively low-interest rates, co-branded credit cards can be more affordable than traditional credit cards. Furthermore, having a co-branded credit card makes it easier to track your spending so you always know exactly how much money you’re putting towards what. This makes budgeting easier since you’ll have all your information together in one place.

Drawbacks Of Using A Co-Branded Credit Card

There are great benefits to using a co-branded credit card, but there are also a few drawbacks it’s best to be aware of before you apply for one of these cards.

One of the biggest drawbacks of using a co-branded credit card is that rewards are limited to just one brand. The rewards are limited to the rules and specifications of the program, even though you can spend your money across the entire network.

And while you’re earning points with every purchase, you may not be able to use your accumulated points right away. Check carefully to see the card’s redemption times, as they may impact your ability to benefit on your next trip or shopping outing.

It’s important to find the best option of a co-branded card that will benefit you the most. There are many co-branded cards available, and it can be confusing, not to mention time-consuming, to get the right card for your needs.

The Best Co-Branded Credit Cards

In its eighth edition market report, Freedonia Group released its picks for the leading co-branded cards as of 2021. The list includes retail, travel, and hospitality industries.

According to the report, the “leading co-branded card issuers” are:

- American Express

- Capital One

- Chase

- Citibank

- Synchrony Financial

The leading airline co-branded card programs are:

- American Airlines

- Delta Air Lines

- JetBlue Airways

- Southwest Airlines

- United Airlines

The leading hotel co-branded card programs are:

- Marriott International

- Hilton Worldwide

- InterContinental Hotels Group

The leading “retail/e-tail store” co-branded card programs are:

- Amazon/Prime

- Costco

- Target

CNBC Select found the “five most unique” co-branded credit cards and provided helpful reviews for each of them:

- Pet lovers can use the American Kennel Club Visa® and earn three points for every dollar spent at the American Kennel Club, pet stores, and vet offices. You’ll also earn two points for every dollar spent on fuel and groceries plus one point for every dollar spent everywhere else Visa is accepted.

- Trekkie fans can apply for NASA Federal Credit Union’s Visa Star Trek Credit Card with four different Star Trek card designs. Once you qualify for the card, you’ll receive three points on merchandise, shows and movies, games, and events purchased at startrek.com. You’ll also be rewarded with two points spent at gas stations and one point on every other purchase.

- Gamers will love the PlayStation® Visa® Credit Card, which lets gaming fans earn five points at the PlayStationTMStore and on every purchase of PlayStation and Sony products. You’ll need to show a purchase confirmation for items purchased at authorized retailers to redeem the points. Also, earn three points on your cell phone bills and one on every other purchase.

- Rail commuters frequently traveling by train will benefit from the Amtrak Guest Rewards® World Mastercard®. It offers great rewards for Amtrak travel as well as any purchases made onboard. You’ll also get a Single-Visit Station Lounge Pass as a reward for opening an account with Amtrak.

- Wine lovers can earn rewards points on purchases at wineries, wine shops, and wine clubs with the Grand Reserve™ World Mastercard®. Apply now, and you’ll earn 50,000 bonus points once you spend $3,000 within 90 days of opening your account. You’ll then qualify to earn seven points per dollar buying wine with the Top Wine Merchant bonus and five points per dollar spent at any of their 450 wineries, wine clubs, and other Grand Reserve Partners. Even if you’re shopping at non-partnered wine or liquor stores, wineries, restaurants, and bars, you’ll still earn three points per dollar spent and, finally, earn two points per dollar spent everywhere else.

If you’re considering getting a co-branded credit card (or any type of credit card), we recommend you view them as a tool to build credit and finance large purchases, not just as a cashless way to spend money you may or may not be able to repay.